What Happens If I Skip EMIs for 3 Months?

|

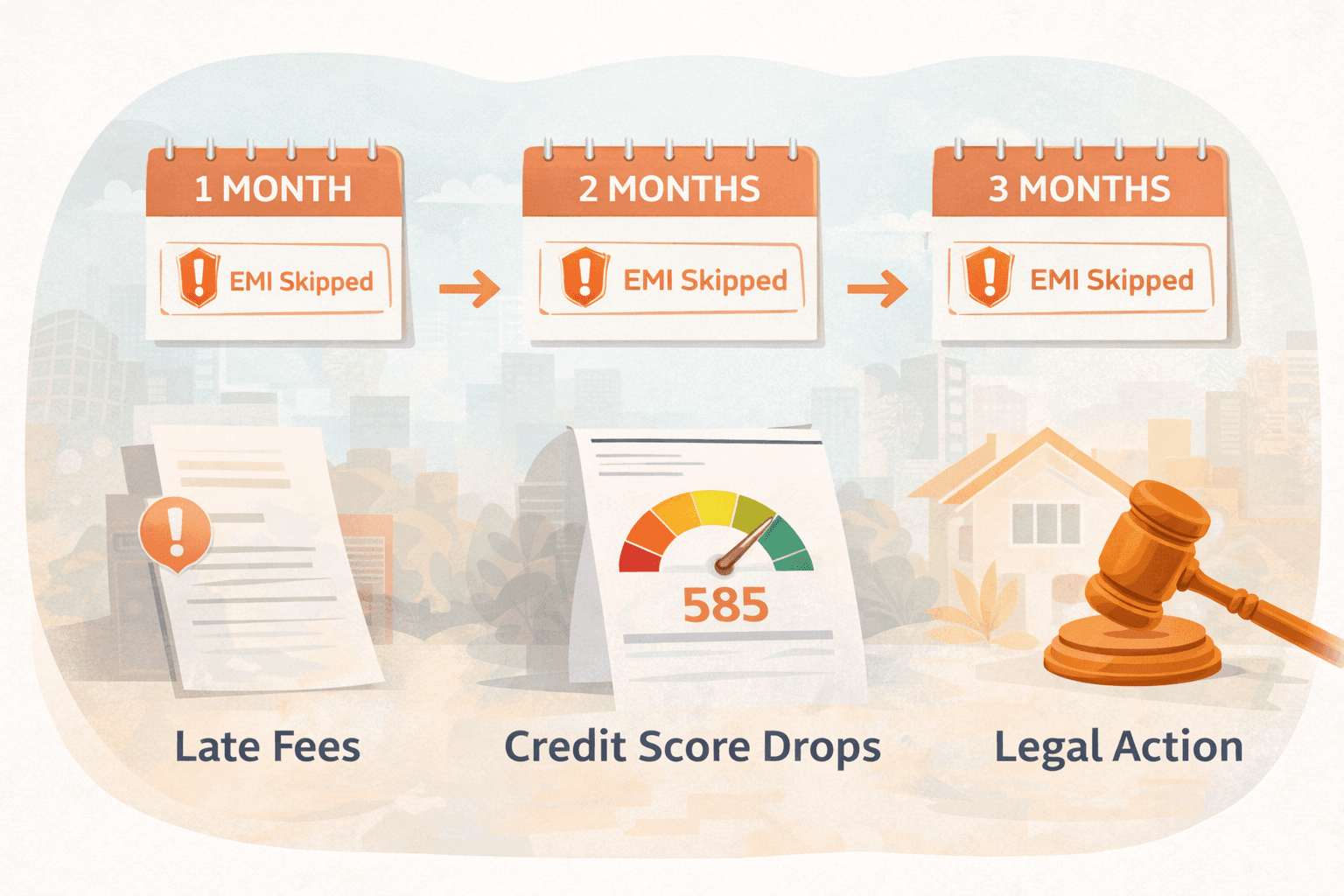

Skipping EMIs for 3 months is not just a delay. It is a serious financial red flag that can impact your credit score, loan status, and future borrowing ability. In India, once your loan crosses 90 days without payment, it is classified as a default under banking norms. This can trigger recovery actions, legal notices, and long-term damage to your credit profile. However, even at this stage, you still have options to recover if you act quickly and strategically. In this guide, we break down exactly what happens when you miss EMIs for 3 months and how you can fix the situation with smart financial decisions and support from Saarathi.ai.

What Does Skipping EMIs for 3 Months Mean

Missing EMIs for 90 days is a critical threshold in the lending system.

RBI Classification Rule

As per the Reserve Bank of India guidelines:

Loans overdue for more than 90 days are classified as Non-Performing Assets (NPA)

This status signals high risk to lenders

At Saarathi.ai, we have observed that many borrowers underestimate this 90-day mark, but it is where consequences sharply escalate.

Immediate Financial Consequences

Accumulation of Penalties

Over 3 months, your dues increase due to:

Late payment fees

Penal interest on overdue EMIs

Compounding charges in some cases

Total Outstanding Becomes Heavier

Instead of just 3 EMIs, you may now owe:

EMI amount x 3

Additional charges

Collection-related costs

Auto-Debit Failures and Bank Charges

Repeated ECS or NACH failures may lead to:

Bank penalties

Reduced account credibility

Credit Score Impact After 3 Missed EMIs

Sharp Drop in Credit Score

Your credit score can drop significantly, often by 100 to 200 points depending on your profile.

Negative Credit History

Your report will reflect:

30, 60, and 90 Days Past Due (DPD)

Default status

Possible “written-off” or “settled” tags later

These records can remain for years and affect all future loan approvals.

According to reporting trends covered in Economic Times and CRISIL insights, prolonged EMI delays are one of the biggest reasons for loan rejection in India.

Legal and Recovery Actions Begin

Recovery Calls and Visits

After multiple missed EMIs:

Recovery agents may start contacting you

Field visits may happen within allowed guidelines

Legal Notices

Lenders may send:

Demand notices

Legal warnings for repayment

Asset Risk for Secured Loans

If your loan is secured (like home loan or loan against property):

The lender can initiate asset seizure under legal procedures

Loan Becomes NPA - What It Means

Loss of Borrower Credibility

Once marked as NPA:

Lenders consider you high risk

Future loan approvals become difficult

Internal Blacklisting by Lenders

Some lenders may:

Restrict future applications

Share risk signals across institutions

Higher Interest Rates in Future

Even if approved later:

You may get loans at higher interest rates

Lower loan amounts may be offered

Can You Still Recover After 3 Missed EMIs

Yes, but immediate action is critical.

Pay Overdue Amount as Soon as Possible

Clearing dues early can:

Stop further penalties

Prevent legal escalation

Request Loan Restructuring

You can ask your lender for:

Lower EMI options

Extended tenure

Temporary relief plans

At Saarathi.ai, we have seen borrowers successfully avoid deeper defaults by restructuring within the 90-day window.

Consider Balance Transfer or Refinance

If your current EMI is too high:

You can compare personal loan offers on Saarathi.ai to find better repayment terms and reduce financial pressure.

Smart Recovery Strategy Using Saarathi.ai

Saarathi Recommendation Engine

This AI system evaluates:

Your financial profile

Repayment capacity

Credit history

It suggests lenders are more likely to approve your application even after delays.

Saarathi Bazaar Dashboard

You can track your application in Saarathi Bazaar and:

Compare multiple offers

Monitor approval status

Choose transparent loan options

AI Expert Support

You can ask eligibility questions via Saarathi AI expert to:

Understand your recovery options

Avoid further mistakes

Plan repayments better

Mistakes to Avoid After Skipping EMIs

Ignoring the Problem

Delays will only increase penalties and legal risk.

Taking High-Interest Emergency Loans

Avoid unregulated lenders offering quick but expensive loans.

Applying Randomly to Multiple Lenders

Multiple rejections further damage your credit profile.

Choosing Settlement Too Early

Settlements hurt your credit score and should be a last resort.

How to Prevent This Situation in Future

Build an Emergency Fund

Keep at least 3 to 6 months of EMI buffer.

Monitor Your Loans Actively

Track all EMIs and due dates.

Borrow Within Your Capacity

Before taking a loan, always compare personal loan offers on Saarathi.ai to ensure affordability.

Use Digital Financial Tools

AI-driven platforms help you stay on top of your repayments and options.

Real Insights from Saarathi.ai

At Saarathi.ai, we have observed that:

Most borrowers recover successfully if they act before 90 days

Early communication with lenders reduces penalties

AI-based loan matching improves approval chances even after setbacks

FAQs

Is missing 3 EMIs considered default?

Yes, after 90 days, your loan is typically classified as a default or NPA.

Can I still pay after 3 months?

Yes, and you should do it immediately to reduce damage.

Will recovery agents visit my home?

They may, but must follow RBI guidelines and respectful conduct.

Can I get another loan after this?

Yes, but it will be harder initially. Smart platforms like Saarathi.ai can help.

Will my credit score recover?

Yes, with consistent repayments over time.

Is loan settlement a good option?

Only as a last resort, as it negatively affects your credit profile.

Conclusion

Skipping EMIs for 3 months is a serious financial situation, but it is still recoverable with the right approach. The key is to act quickly, communicate with your lender, and explore smarter repayment solutions. Ignoring the issue will only make things worse, while timely action can protect your financial future. Saarathi.ai helps you navigate this journey with AI-driven insights, transparent comparisons, and faster approvals. Take control today and discover personalized loan options on Saarathi.ai.