Why Banks Offer Different Rates to Similar Profiles

|

You and your colleague have similar salaries, similar CIBIL scores, and work in the same city. Yet when both of you apply for a loan, the interest rates offered are different. This often confuses borrowers. Why do banks offer different rates to seemingly similar profiles? In 2026, loan pricing is highly data-driven. Interest rates are influenced by multiple visible and invisible factors beyond basic income and credit score. At Saarathi.ai, we have observed that many borrowers assume loan rates are fixed or standardized. In reality, risk-based pricing models determine the final offer. Understanding how lenders calculate interest rates can help you negotiate better and choose smarter.

How Loan Interest Rates Are Determined

Interest rates are based on risk assessment.

Banks and NBFCs evaluate:

CIBIL score

Income stability

Employer category

Existing debt

Loan amount

Tenure

Repayment history

Internal risk models

Even small differences in these factors can lead to rate variation.

Risk-Based Pricing Explained

Most lenders follow risk-based pricing.

This means:

Lower perceived risk = lower interest rate

Higher perceived risk = higher interest rate

Two borrowers may appear similar on the surface but differ in deeper data points.

Factor 1: Credit Score Range, Not Just Score

A score of 750 and 780 are both good. But internally:

780 may qualify for premium rate

750 may fall into slightly higher risk band

Banks divide scores into internal buckets.

Even 10 to 20 point difference can change pricing.

Factor 2: Credit Utilization Ratio

If two borrowers have same income and CIBIL score but:

Borrower A uses 20 percent of credit limit

Borrower B uses 60 percent

Borrower B may receive slightly higher interest rate due to perceived risk.

Credit utilization signals financial stress.

Factor 3: Employer Category and Industry

Banks classify employers into risk tiers.

For example:

Government employees

Large multinational companies

Mid-sized private firms

Self-employed professionals

Stability perception varies.

Even within private sector, industry type matters. IT sector may be treated differently from startup-based employment.

Factor 4: Existing Loan Obligations

Debt-to-income ratio plays a major role.

Two borrowers earning Rs 1 lakh per month:

Borrower A has no existing loans

Borrower B pays Rs 35,000 in EMIs

Borrower B is riskier.

Higher debt burden can increase offered rate.

Factor 5: Loan Tenure and Amount

Longer tenure increases lender risk exposure.

Higher loan amount also increases risk.

Even with similar profiles:

Shorter tenure may attract lower rate

Higher ticket size may push rate upward

Always evaluate tenure impact carefully.

You can compare personal loan offers on Saarathi.ai to see how tenure changes affect total cost.

Factor 6: Relationship With Bank

Existing customers sometimes receive:

Preferential rates

Pre-approved offers

Lower processing fees

Your salary account relationship may influence pricing.

Factor 7: Internal Lending Strategy

Each bank has its own:

Cost of funds

Risk appetite

Growth targets

Portfolio exposure

If a bank is aggressively growing personal loans, rates may be competitive. If exposure is already high, rates may increase.

This is why two banks may offer very different rates for the same borrower.

Factor 8: Market Conditions

Interest rates also depend on:

RBI policy rates

Inflation trends

Liquidity conditions

Economic outlook

Even timing matters. A borrower applying in a rising rate environment may receive higher offer than someone who applied earlier.

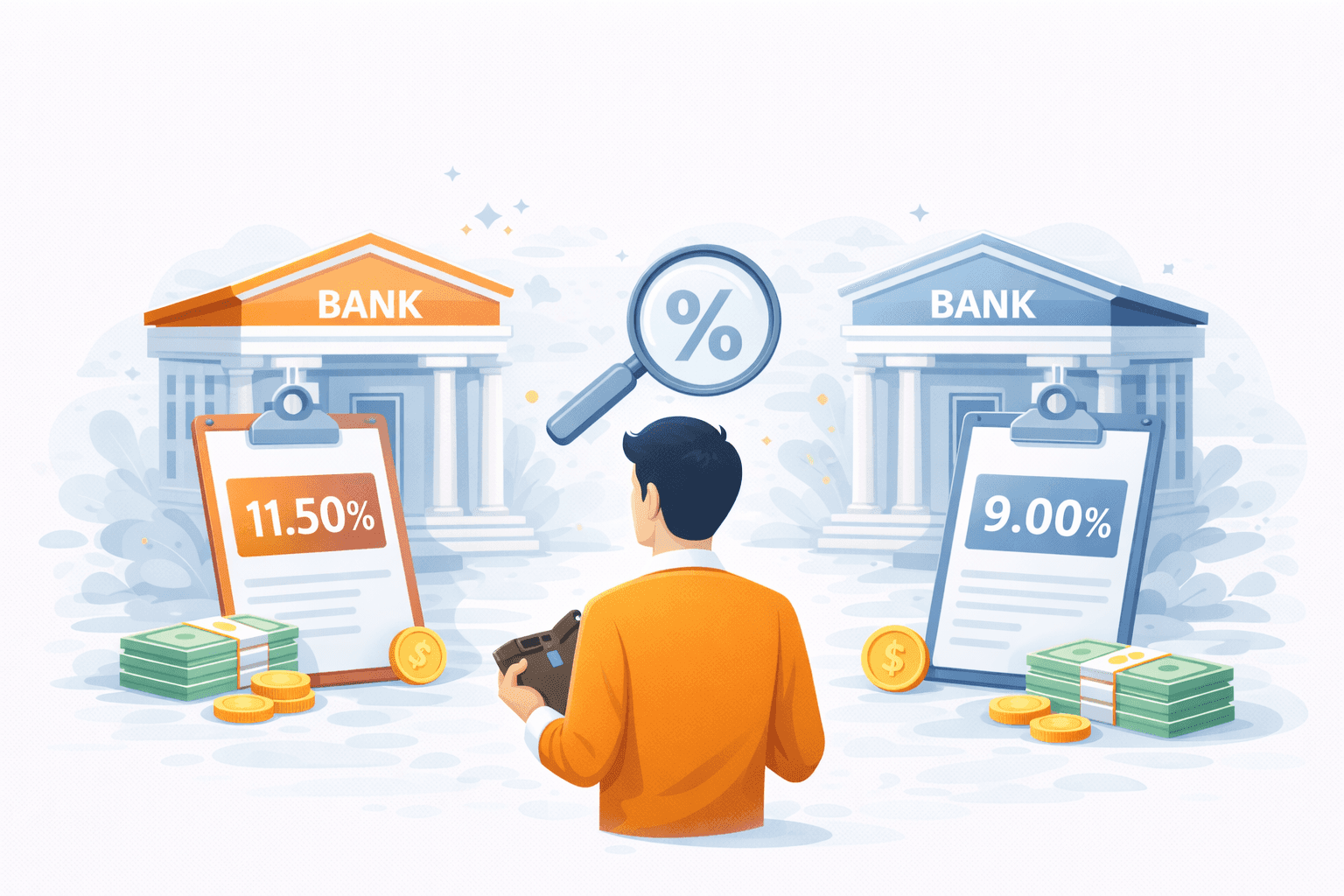

Real Scenario Example

Two salaried professionals:

Profile similarity:

Salary Rs 90,000

CIBIL score above 750

Same city

Differences:

Borrower A credit utilization 25 percent

Borrower B credit utilization 65 percent

Result:

Borrower A receives 11.5 percent

Borrower B receives 13 percent

Small behavioral differences create pricing gaps.

At Saarathi.ai, we have observed that improving even minor risk signals can reduce interest rates meaningfully.

How to Secure a Better Interest Rate

Follow these practical steps:

1. Improve Credit Score Above 780

Higher score increases negotiation power.

2. Reduce Credit Utilization Below 30 Percent

Lower utilization signals stability.

3. Reduce Existing EMIs Before Applying

Improves debt-to-income ratio.

4. Choose Optimal Tenure

Shorter tenure may reduce interest rate.

5. Compare Multiple Lenders

Instead of accepting first offer, compare transparently.

On Saarathi.ai, our Saarathi Recommendation Engine matches you with lenders suited to your profile, helping reduce rejection risk and improve pricing transparency.

You can track offers clearly in Saarathi Bazaar dashboard before making a decision.

Does Negotiation Work?

Yes, sometimes.

If you have:

Strong CIBIL score

Stable income

Good repayment history

You can request rate revision or ask lender to match competitor offer.

However, negotiation works better when you know market rates.

Impact on Long-Term Financial Goals

Even a 1 percent difference in interest rate can significantly affect:

Total repayment

EMI amount

Financial flexibility

For large commitments like housing, comparing home loan offers on Saarathi.ai can help you choose the most competitive structure.

Myth: Same Profile Means Same Rate

This is a common misconception.

Loan pricing is dynamic and multi-layered.

Two profiles may look similar but differ in:

Spending patterns

Internal scoring

Risk segmentation

Market timing

Understanding this prevents frustration.

FAQs

1. Why did my friend get lower rate than me?

Internal risk factors, credit utilization, or debt burden may differ.

2. Can I request lower interest after approval?

You can negotiate before signing agreement.

3. Does applying to multiple banks help?

Excessive applications can hurt credit score. Compare intelligently instead.

4. Does CIBIL score alone determine rate?

No. Many other factors influence pricing.

5. Can refinancing reduce my interest rate?

Yes, if your credit profile improves or market rates decline.

Conclusion

Interest rates are not random. They reflect layered risk assessment.

Key Takeaways:

Small profile differences affect pricing.

Credit utilization and debt ratio matter.

Employer type and tenure influence rates.

Market conditions impact offers.

Comparing lenders improves your chances of better pricing.

Before accepting any loan offer, compare smartly and transparently. Explore personalized loan options on Saarathi.ai today and secure competitive rates with confidence.